Geopolitical Tensions in the Strait of Hormuz: Iran's Naval Drills and Their Ripple Effects on Global Oil Markets

Iran’s naval drills threaten a vital oil chokepoint, spiking prices.

Srinivaasan Balakrishnan

2/19/20263 min read

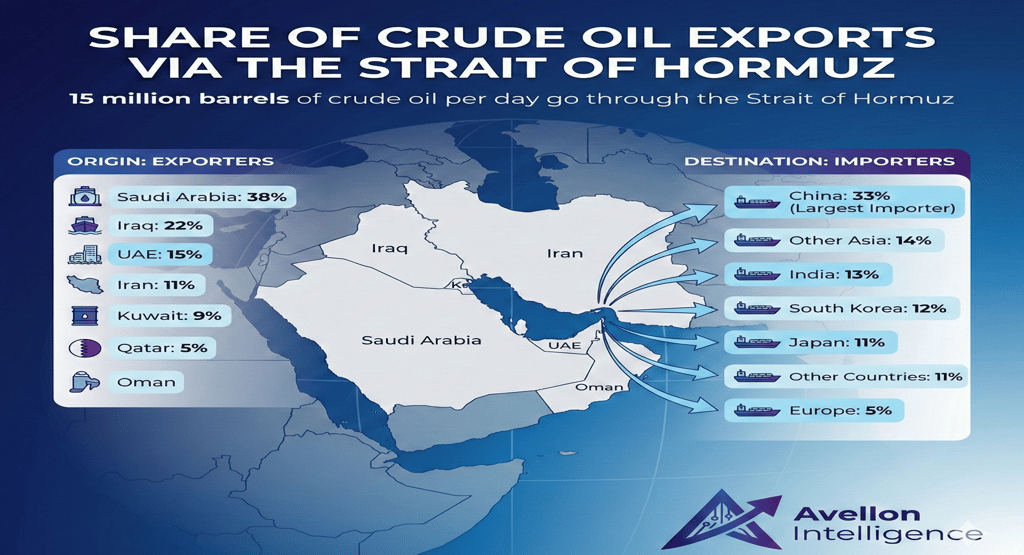

On February 17, 2026, Iran's Islamic Revolutionary Guard Corps (IRGC) conducted live-fire naval exercises titled "Smart Control of the Strait of Hormuz." During the drills, parts of the strait were temporarily closed for several hours due to "security precautions" and to ensure shipping safety. This involved missile launches from coastal and inland positions, advanced armed drones, and operations in signal-jamming conditions. The closure affected sections of this narrow chokepoint, through which approximately 20% of global oil consumption (around 20 million barrels per day) and significant LNG volumes transit, primarily from Saudi Arabia, Iraq, the UAE, Kuwait, and Qatar.

The event coincided with indirect U.S.-Iran nuclear talks in Geneva and followed recent U.S. military deployments in the region. While no full blockade occurred and traffic resumed after the drills, the announcement represented a rare step, Iran's first declared partial shutdown in decades, serving as a demonstration of control amid heightened geopolitical tensions. Iran has also announced upcoming joint naval maneuvers with Russia in the Gulf of Oman and northern Indian Ocean.

Market Reaction: Crude Oil Prices The brief disruption triggered an immediate risk premium in oil markets. On February 18, 2026, Brent crude futures rose approximately 4.35% to settle around $70.35 per barrel, while WTI advanced 4.59% to $65.19 per barrel. This rebound reflected market sensitivity to chokepoint vulnerabilities, despite no sustained supply interruption.

Recent price movements show volatility tied to the event:

Brent crude hovered near $69–$71 in mid-February, with spot levels around $69.01–$70.35 post-event.

WTI reached $65.01 in some reports, up over 4% amid escalation fears.

Analysts note that while the closure was short-lived, repeated or extended actions could add 15–20% to prices in a worst-case scenario. However, global oversupply concerns and diplomatic channels have limited sustained upside, with forecasts for 2026 averaging $56–$65 per barrel under baseline assumptions.

Freight Rates: Tanker Market Dynamics Tanker rates on key routes remained elevated but showed mixed movements in mid-February 2026. VLCC rates for the Middle East Gulf to China (TD3C, 270,000mt) stood at WS132.78, equating to a time charter equivalent (TCE) of approximately $117,360 per day—down slightly from recent peaks but still reflecting geopolitical premiums and longer voyages.

Other segments:

West Africa to China (TD15, 260,000mt): WS121.44, TCE around $103,700/day.

Nigeria to UK Continent (TD20, 130,000mt Suezmax): WS157.78, TCE near $69,900/day.

Clean tanker rates retreated in some areas, with Persian Gulf to Japan LR2 routes declining.

The brief Hormuz restriction caused minor delays to inbound shipping but no major rerouting. Ongoing factors like sanctions, supply shifts, and strategic hoarding continue to support firm dirty tanker earnings.

Insurance and Risk Premiums War-risk insurance for vessels transiting the Middle East Gulf and Hormuz area has risen amid tensions. Premiums quoted around 0.5% of hull value (up from 0.2–0.3% in prior periods), adding significant daily costs for large tankers—tens of thousands of dollars per voyage. Even short exercises like this prompt underwriters to reassess exposure, contributing to "coercion creep" in maritime risk pricing.

Broader Implications This drill highlighted the strait's fragility: at its narrowest, only about 21 miles wide with two-mile shipping lanes. No actual supply shock materialized, but the event reminded markets of potential disruptions to flows from key producers. Pipeline alternatives provide partial mitigation, though capacity limits their effectiveness in a prolonged scenario.

Forward curves indicate mild contango, with geopolitical risks providing intermittent support against oversupply pressures. Monitoring nuclear talks, U.S. military postures, and any follow-on exercises (including Iran-Russia drills) remains critical for near-term sentiment.

In summary, the temporary closure acted as a strategic signal rather than a direct supply threat, embedding a modest risk premium in prices and rates. Absent escalation, markets are likely to stabilize, though chokepoint vulnerabilities ensure ongoing sensitivity to Middle East developments.

About the author: Srinivaasan Balakrishnan is Co-Founder of Avellon Intelligence and Director at Indic Researchers Forum (IRF), columnist and author decoding war, trade, and global supply chains. Reached in X: @Srinivstrat

Contact

Connect with us for enterprise risk solutions

© 2026. All rights reserved.